Destination switching is redrawing global travel map

Globetrender’s Executive Travel Pulse survey of globally informed C-suite and director-level executives across the industry reveals that the defining behavioural shift triggered by the Middle East conflict isn’t cancellations, but destination switching – with a new set of unexpected winners coming into focus. Robbie Hodges reports

Globetrender’s research in brief:

- 44% of executives cite destination switching as the primary behavioural shift among travellers

- 34% report cancellations, while 12% note shorter booking windows

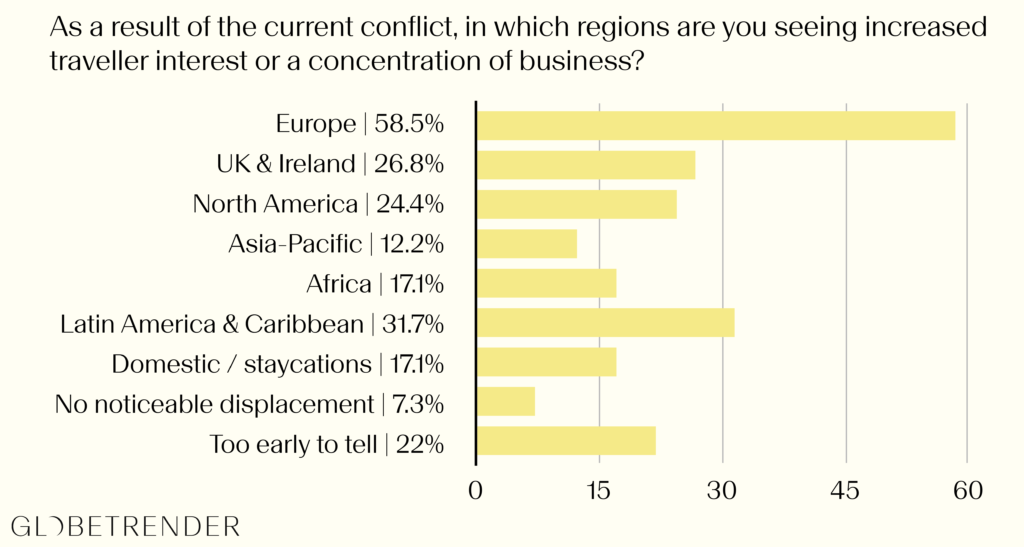

- 59% see increased demand for Europe; 32% report growth in Latin America & the Caribbean; 27% cite uplift in the UK & Ireland and 24% in North America

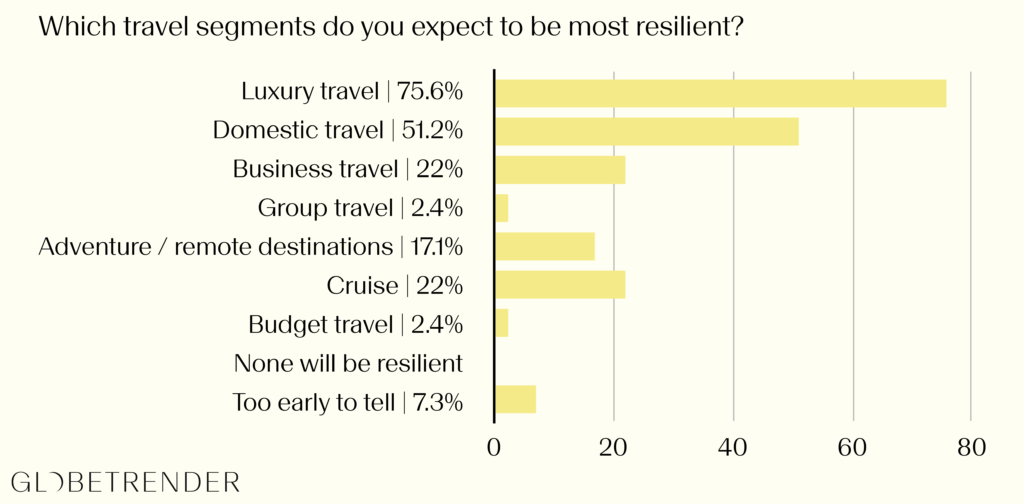

- 76% identify luxury travel as the most resilient segment, followed by domestic travel (51%) and cruise (22%) – with just 2% viewing the budget sector as resilient

With limited reliable data on travel industry sentiment towards the ongoing conflict in the Middle East, we turned to our network of C-suite and director-level travel leaders to understand how the ongoing conflict is shaping consumer behaviour and business strategy. This is one of three dispatches drawn from the findings, with the remaining two linked at the end of the article.

When asked which changes they’re seeing in consumer behaviour, 44% of responses mentioned destination switching as the most notable change they’ve seen since conflict in the Middle East accelerated in late February/March, ahead of cancellations (34%) and shorter booking windows (12%). In other words, travel demand is proving resilient, but increasingly fluid.

Rather than abandoning trips, travellers are gravitating towards destinations that are perceived as safer or more accessible in terms of flight routings. For global brands, this creates an opportunity to absorb displaced demand, while smaller, regionally focused players face greater risk. One response could be collaboration: forming partnerships to redirect guests to alternative destinations, retaining relationships and unlocking new revenue streams until conditions stabilise.

If travellers are switching, where are they going? Europe is the primary beneficiary, with 59% of respondents reporting increased interest in the region. Southern Europe in particular is already seeing anecdotal uplift.

Meanwhile, 32% of executives report seeing increased demand in Latin America and the Caribbean, while the UK & Ireland (27%) and North America (24%) are also capturing displaced demand. North America’s position is particularly notable given its recent decline in inbound appeal.

As highlighted in Globetrender’s Anti-Americana report for VOLT members, overseas arrivals to the US fell in 2025, with Reuters reporting a 2.8% drop in May alone, including a 4.4% decline from Western Europe. That North America is now re-emerging as a fallback destination is indicative of a fundamental behavioural truth – in times of uncertainty, the familiar regains its value.

When it comes to resilience, the hierarchy of travel segments is becoming more pronounced. Luxury travel leads, with 76% of respondents identifying it as the most resilient sector – perhaps unsurprising given its high margins and affluent customer base. Domestic travel follows at 51%, while cruise (22%) emerges in third place as a quietly robust category. At the other end of the spectrum, budget travel lags significantly, with just 2% of executives viewing it as resilient.

This divergence reflects a budget-luxury gap in the industry that has been widening since the Covid-19 pandemic. As geopolitical instability persists, investment continues to concentrate further at the premium end, while lower-cost travel options face increasing pressure.

The data points to a clear conclusion: this is not a demand crisis, but a redistribution of global travellers. Even if the conflict proves short-lived, the ripple effects could endure, reshaping where capital flows and reinforcing investment in already wealthy regions and segments perceived as more “shockproof”.

Globetrender has a suite of products and services designed to help travel leaders better anticipate and prepare for future disruption, from workshops to intelligence subscriptions. Reach out to discuss how we might be able to help.

Explore the full findings of Globetrender's Executive Travel Pulse

- Travel execs remain hopeful amid Middle East conflict

- Strategic foresight gains urgency amid Middle East conflict

Methodology

Globetrender surveyed 41 senior travel industry leaders from globally operating brands, with 63% of respondents at C-suite level (including CEOs and founders) and a further 32% at director level. The 20-question online survey was conducted in March 2026, capturing perspectives across sectors including hospitality, aviation, travel technology and tour operations.

Responses were anonymised and analysed to identify key quantitative trends and emerging qualitative insights, reflecting industry sentiment at a specific moment in time amid ongoing geopolitical uncertainty.